For my readers, I apologised for the quiet month of blogging.

It is a busy month of flying across the continents! Finally, I am home today after more than

ten days abroad in UK and Brazil. The traveling were not made any easier, with more

than twenty-five hours of air travel single-way Brazil-Singapore not to mention

additional hours spent on the roads and hang around at airport. Instead of snoozing during the travel and wait, I actually drafted few blog articles. Below

is one.

It is a busy month of flying across the continents! Finally, I am home today after more than

ten days abroad in UK and Brazil. The traveling were not made any easier, with more

than twenty-five hours of air travel single-way Brazil-Singapore not to mention

additional hours spent on the roads and hang around at airport. Instead of snoozing during the travel and wait, I actually drafted few blog articles. Below

is one.

Brief

Earlier,

I had blogged about China titanic advancement in the last decade and why I am bullish

on its long term economic outlook. With this positive appraisal in mind, it is

not surprising that I added a stock counter with China exposure lately. The

company is CapitaRetail China Trust

(SGX: AU8U) “CRCT” listed in SGX, owned 21.3% by CapitaMalls Asia as of end last

year. CapitaMalls Asia was taken private few months ago by CapitaLand (SGX: C31), South

East Asia largest listed Real Estate Company.

I had blogged about China titanic advancement in the last decade and why I am bullish

on its long term economic outlook. With this positive appraisal in mind, it is

not surprising that I added a stock counter with China exposure lately. The

company is CapitaRetail China Trust

(SGX: AU8U) “CRCT” listed in SGX, owned 21.3% by CapitaMalls Asia as of end last

year. CapitaMalls Asia was taken private few months ago by CapitaLand (SGX: C31), South

East Asia largest listed Real Estate Company.

CRCT is

the first and only PRC shopping mall REIT in Singapore. It has a portfolio of

10 income-producing shopping malls in six of China’s cities including 5 malls

in Beijing (78% of portfolio) and one each in Shanghai, Henan, Inner Mongolia,

Anhui and Hubei province. Total GRA is approx. 605k sqm with over 70 million of

shopper traffic. All the malls are located in populous areas that are

accessible to major transportation routes or access points. Below are more

informations on the various malls within CRCT including their portfolio valuation.

the first and only PRC shopping mall REIT in Singapore. It has a portfolio of

10 income-producing shopping malls in six of China’s cities including 5 malls

in Beijing (78% of portfolio) and one each in Shanghai, Henan, Inner Mongolia,

Anhui and Hubei province. Total GRA is approx. 605k sqm with over 70 million of

shopper traffic. All the malls are located in populous areas that are

accessible to major transportation routes or access points. Below are more

informations on the various malls within CRCT including their portfolio valuation.

Strong Fundamentals

In

the last 12 months, CRCT stock price range from a minimum of S$1.40 during end

Jan 2014 to a maximum of S$1.70 during end Aug about two months ago. It settles

at S$1.60 currently with a market cap of S$1.3b. CRCT

has strong support from its Temasek backed CapitaLand with healthy fundamentals.

Latest Price to Book ratio is 1.05 with dividend yield of 6.2% based on

annualised 1H2014 DPU of 4.99Sc. Based on 1H14 results, gearing is 29.8% with

an average debt of cost of 3.6% mostly fixed and well distributed for the next

few years. Interest coverage is healthy at 5.5x and occupancy of its malls are strong

at 98% capacity.

the last 12 months, CRCT stock price range from a minimum of S$1.40 during end

Jan 2014 to a maximum of S$1.70 during end Aug about two months ago. It settles

at S$1.60 currently with a market cap of S$1.3b. CRCT

has strong support from its Temasek backed CapitaLand with healthy fundamentals.

Latest Price to Book ratio is 1.05 with dividend yield of 6.2% based on

annualised 1H2014 DPU of 4.99Sc. Based on 1H14 results, gearing is 29.8% with

an average debt of cost of 3.6% mostly fixed and well distributed for the next

few years. Interest coverage is healthy at 5.5x and occupancy of its malls are strong

at 98% capacity.

Diversified Tenant Base

CRCT

malls have a mix of Master and Multi-tenanted leases profile. Master lease

is of typical 20 years to ensure stable cash flow. Multi-tenanted leases

provide growth and include Anchor Tenant lease which is 15-20 years;

Mini-anchor tenants 5-7 years and Specialty tenants up to 3 years. As of 1H14,

there are 3 Master-Leased malls which contribute 22% of NPI and 7

Multi-tenanted malls accounting for 78% of NPI.

malls have a mix of Master and Multi-tenanted leases profile. Master lease

is of typical 20 years to ensure stable cash flow. Multi-tenanted leases

provide growth and include Anchor Tenant lease which is 15-20 years;

Mini-anchor tenants 5-7 years and Specialty tenants up to 3 years. As of 1H14,

there are 3 Master-Leased malls which contribute 22% of NPI and 7

Multi-tenanted malls accounting for 78% of NPI.

CRCT

tenants include big names like Wal-Mart, Carrefour and the Beijing Hualian

Group (BHG) under master leases or long-term leases. The anchor tenants are

UNIQLO, ZARA, Vero Moda, Sephora, Watsons, KFC, Pizza Hut and BreadTalk.

tenants include big names like Wal-Mart, Carrefour and the Beijing Hualian

Group (BHG) under master leases or long-term leases. The anchor tenants are

UNIQLO, ZARA, Vero Moda, Sephora, Watsons, KFC, Pizza Hut and BreadTalk.

The two Tenants in the month of Dec 2013 in terms of Total Rental income are 1) BHG

occupies 41.3% of Total committed Gross Rentable Area (GRA) and contributes to

22.9% of Total Rental Income. 2) Carrefour Supermarket occupies 10.7% of

committed GRA and contributes 4% of Total Rental Income.

occupies 41.3% of Total committed Gross Rentable Area (GRA) and contributes to

22.9% of Total Rental Income. 2) Carrefour Supermarket occupies 10.7% of

committed GRA and contributes 4% of Total Rental Income.

The rest

of the tenants all contribute 4% or less of the Total Rental Income which gives

CRCT a well diversify low risk spread of tenants.

of the tenants all contribute 4% or less of the Total Rental Income which gives

CRCT a well diversify low risk spread of tenants.

Potential Upside

Near term growth stems from the recently revamped CapitaMall

Minzhongleyuan mall opened 1 May 2014. Also CapitaMall Grand Canyon mall that

was acquired in 1H13 is also expected to have its NPI raised by end-2014 due to

new lease signed at higher rents. In the longer term, CRCT can tap on ROFR

acquisition of CapitaMalls Asia assets granted by various CapitaMalls Asia

funds.

Minzhongleyuan mall opened 1 May 2014. Also CapitaMall Grand Canyon mall that

was acquired in 1H13 is also expected to have its NPI raised by end-2014 due to

new lease signed at higher rents. In the longer term, CRCT can tap on ROFR

acquisition of CapitaMalls Asia assets granted by various CapitaMalls Asia

funds.

CapitaMall

Anzhen, CapitaMall Erqi and most of CapitaMall Shuangjing’s GRA are contracted

under master lease, which has provisions for increase of rental revenues

through step-ups in the base rent. In addition, master leased malls also

provide further potential upside through a percentage of tenants’ sales

turnover if the turnover exceeds an agreed threshold. Similarly, most of the

leases for the anchor, mini-anchors and specialty tenants have clauses with

annual step-up in the base rent and include provisions for rent to be payable

at the then applicable base rent or at a percentage of sales turnover,

whichever is the higher.

Anzhen, CapitaMall Erqi and most of CapitaMall Shuangjing’s GRA are contracted

under master lease, which has provisions for increase of rental revenues

through step-ups in the base rent. In addition, master leased malls also

provide further potential upside through a percentage of tenants’ sales

turnover if the turnover exceeds an agreed threshold. Similarly, most of the

leases for the anchor, mini-anchors and specialty tenants have clauses with

annual step-up in the base rent and include provisions for rent to be payable

at the then applicable base rent or at a percentage of sales turnover,

whichever is the higher.

So

far, CRCT had enjoyed healthy portfolio rental reversion of 24.9% as of 1H14.

far, CRCT had enjoyed healthy portfolio rental reversion of 24.9% as of 1H14.

Rolf’s View

China

rapid urbanization is definitely going to spur CRCT long term business

prospects.

rapid urbanization is definitely going to spur CRCT long term business

prospects.

Having

seen myself and heard from my China friends, well-accessible malls in the cities

are always busy and crowded. People in China love to shop! While the older

Chinese generation are generally savers, the younger generations tend to spend

more relative to their income.

seen myself and heard from my China friends, well-accessible malls in the cities

are always busy and crowded. People in China love to shop! While the older

Chinese generation are generally savers, the younger generations tend to spend

more relative to their income.

In

view of the growing population and scarce land in bigger cities in China, property

asset re-valuation upward potential is high.

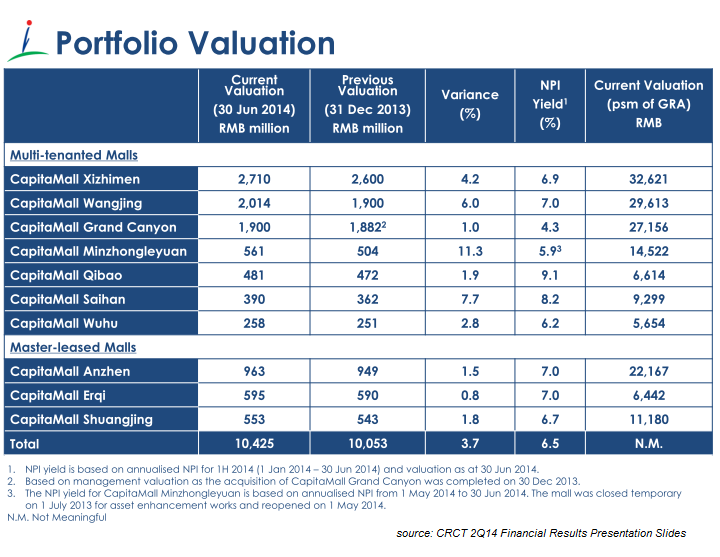

For the record, as of 1H14 compared to half year ago, CRCT’s portfolio

valuation rose 3.7%.

view of the growing population and scarce land in bigger cities in China, property

asset re-valuation upward potential is high.

For the record, as of 1H14 compared to half year ago, CRCT’s portfolio

valuation rose 3.7%.

Of course

not everything is smooth sailing. China is anticipated to experience decelerated

economic growth than before, with loan default hard landing problems on the

headlines speculated by many investors. The potential rising interest rate environment

is not making it any easier too for CRCT future acquisition plans.

not everything is smooth sailing. China is anticipated to experience decelerated

economic growth than before, with loan default hard landing problems on the

headlines speculated by many investors. The potential rising interest rate environment

is not making it any easier too for CRCT future acquisition plans.

Moreover, 87%

of CRCT’s Total Rental Income is coming from committed leases with turnover

rent provisions. There will be a danger of sales decline affecting the company

rental income.

of CRCT’s Total Rental Income is coming from committed leases with turnover

rent provisions. There will be a danger of sales decline affecting the company

rental income.

Related Posts:

There is actually another PRC shopping mall trust listed in Singapore – Perennial Retail China Trust (PRCT).

Hi S-Reit SI,

Thanks for the comments.

If I am not wrong, PRCT is a Business Trust where I mentioned CRCT is the only China mall REIT listed in SGX.

Correct me if I am wrong.

For difference between Business Trust and REIT, you can refer to my earlier post link https://rolfsuey.com/2014/03/reits-or-business-trust.html?m=1

Rolf

Ah yes, you're right. PRCT is listed as a property trust, not a REIT. Thanks for pointing it out. 🙂

Hi S-Reit SI,

No problem, small hiccup. In fact I appreciate your pointer as it makes me look into PRCT.

By the way, do you have a blog yourself for my reading? Thanks.

Rolf

I'm not really an active blogger. You can find my blog here:

http://sreitsysteminvestor.blogspot.sg

Cheers!